We solve a time series prediction problem by training multiple models ( statsmodels.tsa and xgboost) using the Azure ML Service.

-

Create a

.envfile with the same content as.env.sample.source .env -

Build a docker image:

docker build -f Dockerfile -t rossmann_img:0.1 . -

Test the image and the model:

docker run -it --rm --name delete_me \ -v "$(pwd)":/home/rossmann \ -v "$(pwd)/../data":/home/data \ -w /home/rossmann \ rossmann_img:0.1 /bin/bash # Inside the image /opt/conda/envs/rossmann/bin/python train/train_01.py \ --data_dir ../data/rossmann-store-sales/source \ --max_pdq 4 1 2 \ --n_stores 4You can test the the other models in the same way: just look in

train/train_XY.pyunderif __name__ == '__main__':to see an example how the model can be tested locally before submitting it to a remote compute instance. -

Push the image to a container registry (AML or Dockerhub):

Login to an AML container registry:

docker login -u "$AML_CONTAINER_REGISTRY_USR" \ -p "$AML_CONTAINER_REGISTRY_PWD" \ $AML_CONTAINER_REGISTRY_SERVER

or to Docker hub:

docker login -u "$DOCKER_HUB_USR" \ -p "$DOCKER_HUB_PWD"

-

Tag the image and add it to the container registry:

docker tag rossmann_img:0.1 $AML_CONTAINER_REGISTRY_SERVER/rossmann_img:0.1 docker push $AML_CONTAINER_REGISTRY_SERVER/rossmann_img:0.1

Look at this notebook for more information how to use Azure ML Service for model deployment.

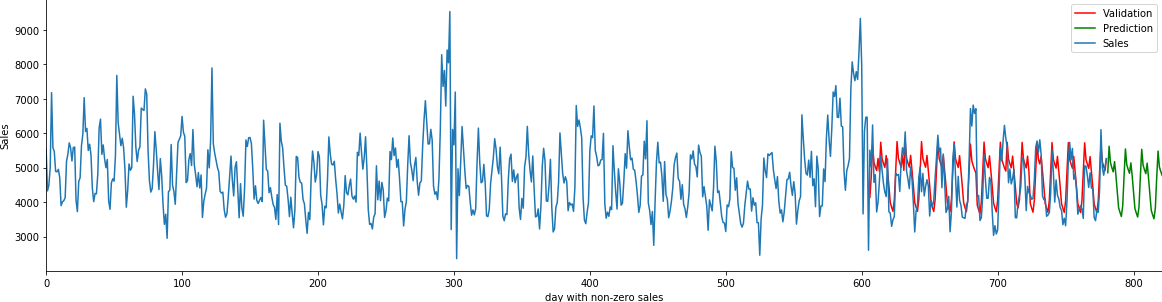

We fit an individual SARIMAX model for every store. Some relevant steps:

-

Remove items from the sequence where the store is closed and

sales=0. An exogen variableis_closedcan not completely compensate the effect of rapidly falling values of the time series to zero since it has an additive effect to the final outcome. -

Transform

Datetodays_since_startand remove the trend option for the SARIMAX models (i.e. usetrend='c'instead oftrend='ct') -

Do not use any periodicity options since a lot of data points are "missing" due to holidays.

-

Hyperparameter selection. For every model pick the best (p,d,q) values from a predefined grid. For every combination we train a model in the interval [2013-01-01 : 2014-12-31] and use the prediction for the interval [2015-01-01 : 2015-07-31] to select the best (p,d,q). At the moment, we use the mean absolute error metric but code can be easily modified to use some information criteria or another metric.

Since this approach is extremely popular, I have added it. Variations of the implementations of this model can be found here.