(ICLR'24) Rethinking Channel Dependence for Multivariate Time Series Forecasting: Learning from Leading Indicators

This repo is the official Pytorch implementation of Rethinking Channel Dependence for Multivariate Time Series Forecasting: Learning from Leading Indicators.

- Rethinking channel dependence in MTS from a perspective of lead-lag relationships.

- Reasoning why CD models show inferior performance.

- Many variates are unaligned with each other, while traditional models (e.g., Informer) simply mix multivariate information at the same time step. Thus they introduce outdated information from lagged variates which are noise and disturb predicting leaders.

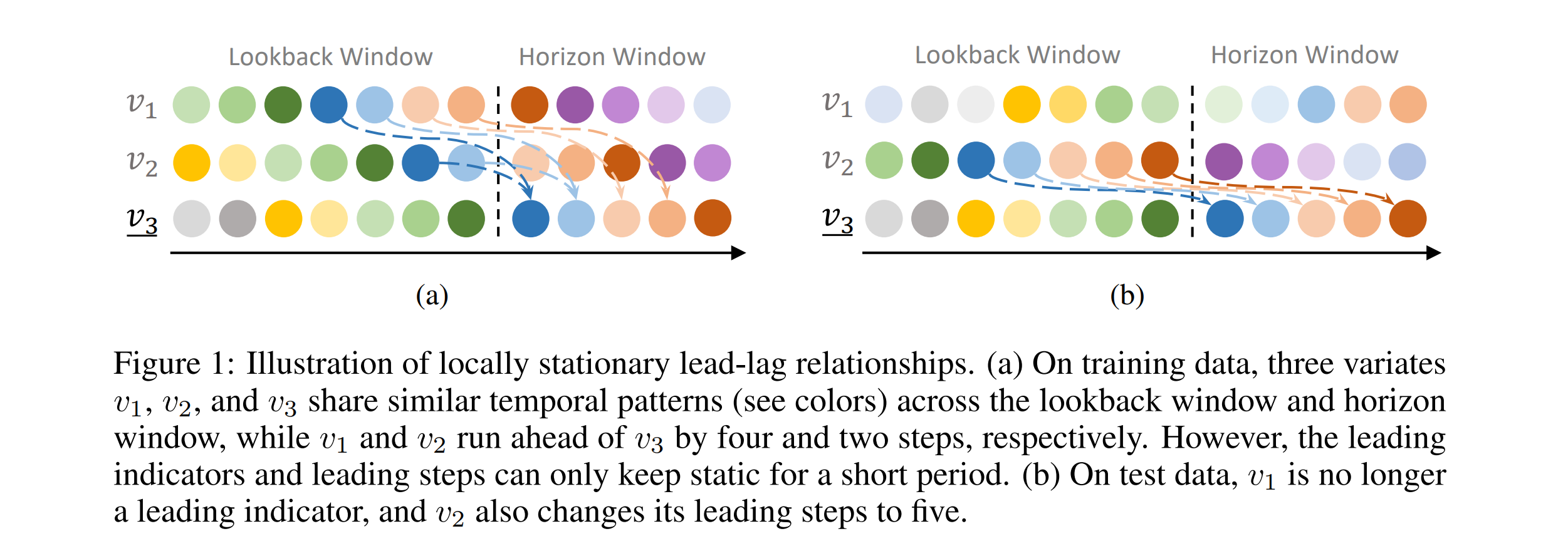

- Though other models (e.g., Vector Auto-Regression) memorize CD from different time steps by static weights, they can suffer from overfiting since the leading indicators and leading steps vary over time.

- Alleviating distribution shifts by dynamically selecting and shifting indicators.

- Recent works (e.g., instance normalization methods) focus on distribution shifts in statistical properties (e.g., mean and variance). We take a novel investigation into a different kind of distribution shifts in channel dependence.

- As the leading indicators vary over time, we evaluate all pairs between variates as fast as possible and dynamically select a subset from all variates. After the coarse selection, we design a neural network to finely model the channel dependence within the small subset.

- As the leading steps vary over time, we dynamically shift the selected indicators to get aligned with the target variate, mitigating the varying misalignment.

- A lightweight yet strong baseline for MTS forecasting.

- We propose a parameter-efficient baseline named LightMTS. With the parameter efficiency close to DLinear, LightMTS outperforms DLinear by a large margin and achieves SOTA performance on several benchmarks.

An example:

python -u run_longExp.py --dataset Weather --model DLinear --lift --seq_len 336 --pred_len 96 --leader_num 4 --state_num 8 --learning_rate 0.0005The scripts/ directory contains our scripts for re-experiments but does not cover all datasets.

We slightly revised our method after the paper submission, while we have not re-run all experiments yet due to limited computing resources.

You can perform hyperparameter tuning on your own if necessary.

It is recommended to obtain a pretrained and frozen backbone first, in order to reduce the time cost of

selecting LIFT's hyperparameters. (Add args --pretrain --freeze into your scripts to load a frozen backbone.)

Our implementation precomputes the leading indicators and the leading steps at all time steps over the dataset, which are saved to the prefetch/ directory.

Given a frozen backbone, we also precompute the backbone's predictions only once and save them to the results/ directory.

The LIFT module directly takes in the tensors of predictions without recomputing the lead-lag relationships (and the backbone's prediction if --pretrain --freeze).

To avoid repeatedly loading the input tensors from RAM to GPU memory, we keep all the input tensors on the GPU memory by default.

You can set --pin_gpu False if your GPU memory is limited.

All benchmarks can be downloaded from Google Drive.

pip3 install -r requirements.txtIf you find this useful for your work, please consider citing it as follows:

@inproceedings{

LIFT,

title={Rethinking Channel Dependence for Multivariate Time Series Forecasting: Learning from Leading Indicators},

author={Lifan Zhao and Yanyan Shen},

booktitle={The Twelfth International Conference on Learning Representations},

year={2024},

url={https://openreview.net/forum?id=JiTVtCUOpS}

}