This project

- is stable and being incubated for long-term support. It may contain new experimental code, for which APIs are subject to change.

- requires PyStan as a system dependency. PyStan is licensed under GPLv3, which is a free, copyleft license for software.

Orbit is a Python package for Bayesian time series forecasting and inference. It provides a familiar and intuitive initialize-fit-predict interface for time series tasks, while utilizing probabilistic programming languages under the hood.

Currently, it supports concrete implementations for the following models:

- Exponential Smoothing (ETS)

- Damped Local Trend (DLT)

- Local Global Trend (LGT)

- Kernel Time-based Regression (KTR-Lite)

It also supports the following sampling methods for model estimation:

- Markov-Chain Monte Carlo (MCMC) as a full sampling method

- Maximum a Posteriori (MAP) as a point estimate method

- Variational Inference (VI) as a hybrid-sampling method on approximate distribution

Install from PyPi:

$ pip install orbit-mlInstall from source:

$ git clone https://github.com/uber/orbit.git

$ cd orbit

$ pip install -r requirements.txt

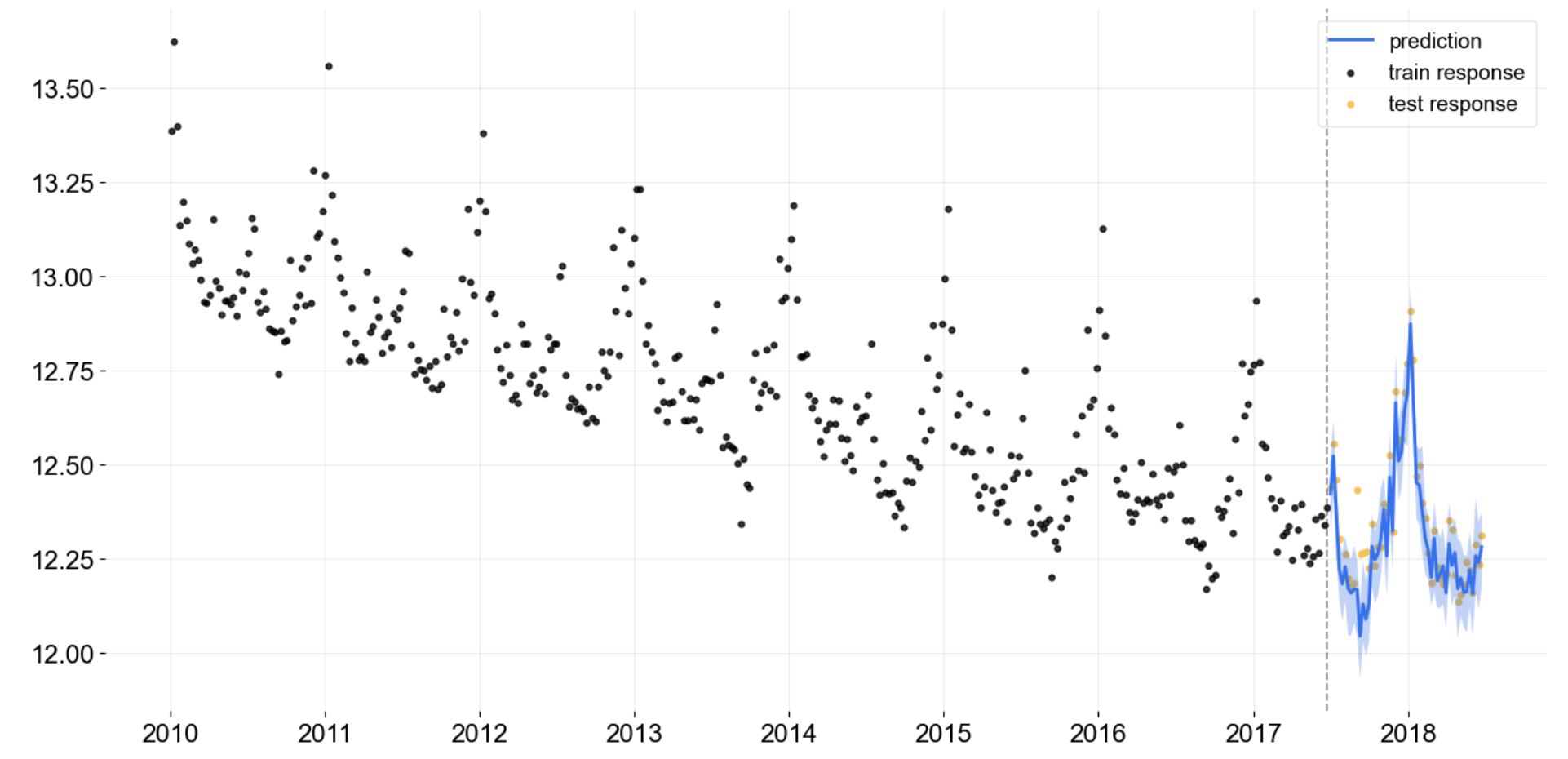

$ pip install .$ pip install git+https://github.com/uber/orbit.git@devfrom orbit.utils.dataset import load_iclaims

from orbit.models.dlt import DLTFull

from orbit.diagnostics.plot import plot_predicted_data

# log-transformed data

df = load_iclaims()

# train-test split

test_size = 52

train_df = df[:-test_size]

test_df = df[-test_size:]

dlt = DLTFull(

response_col='claims', date_col='week',

regressor_col=['trend.unemploy', 'trend.filling', 'trend.job'],

seasonality=52,

)

dlt.fit(df=train_df)

# outcomes data frame

predicted_df = dlt.predict(df=test_df)

plot_predicted_data(

training_actual_df=train_df, predicted_df=predicted_df,

date_col=dlt.date_col, actual_col=dlt.response_col,

test_actual_df=test_df

)

More examples can be found under tutorials and examples.

A backtest demo:

We welcome community contributors to the project. Before you start, please read our code of conduct and check out contributing guidelines first.

We document versions and changes in our changelog.

- HTML documentation (stable): https://orbit-ml.readthedocs.io/en/stable/

- HTML documentation (latest): https://orbit-ml.readthedocs.io/en/latest/

- HTML documentation (deprecated): https://uber.github.io/orbit/

To cite Orbit in publications, refer to the following whitepaper:

Orbit: Probabilistic Forecast with Exponential Smoothing

Bibtex:

@misc{

ng2020orbit,

title={Orbit: Probabilistic Forecast with Exponential Smoothing},

author={Edwin Ng,

Zhishi Wang,

Huigang Chen,

Steve Yang,

Slawek Smyl},

year={2020}, eprint={2004.08492}, archivePrefix={arXiv}, primaryClass={stat.CO}

}

- Bingham, E., Chen, J. P., Jankowiak, M., Obermeyer, F., Pradhan, N., Karaletsos, T., Singh, R., Szerlip, P., Horsfall, P., and Goodman, N. D. Pyro: Deep universal probabilistic programming. The Journal of Machine Learning Research, 20(1):973–978, 2019.

- Hoffman, M.D. and Gelman, A. The No-U-Turn sampler: adaptively setting path lengths in Hamiltonian Monte Carlo. J. Mach. Learn. Res., 15(1), pp.1593-1623, 2014.

- Hyndman, R., Koehler, A. B., Ord, J. K., and Snyder, R. D. Forecasting with exponential smoothing: the state space approach. Springer Science & Business Media, 2008.

- Smyl, S. Zhang, Q. Fitting and Extending Exponential Smoothing Models with Stan. International Symposium on Forecasting, 2015.