Welcome to the Risk Management Analytics repository! This collection of R scripts and techniques is tailored for financial professionals, risk analysts, and enthusiasts seeking powerful tools for assessing and managing financial risks. Leverage the capabilities of R to enhance your risk management strategies with a focus on key techniques such as:

- Value-at-Risk (VaR): Gauge the potential loss under normal market conditions at a specified confidence level using both historical and parametric methods.

- Expected Shortfall (ES): Go beyond VaR by estimating the average loss in the tail of the distribution, providing a more comprehensive measure of risk.

- Multi-Asset Value-at-Risk: Extend risk assessment to multi-asset portfolios, incorporating correlations and dependencies to capture the intricacies of diversified investments.

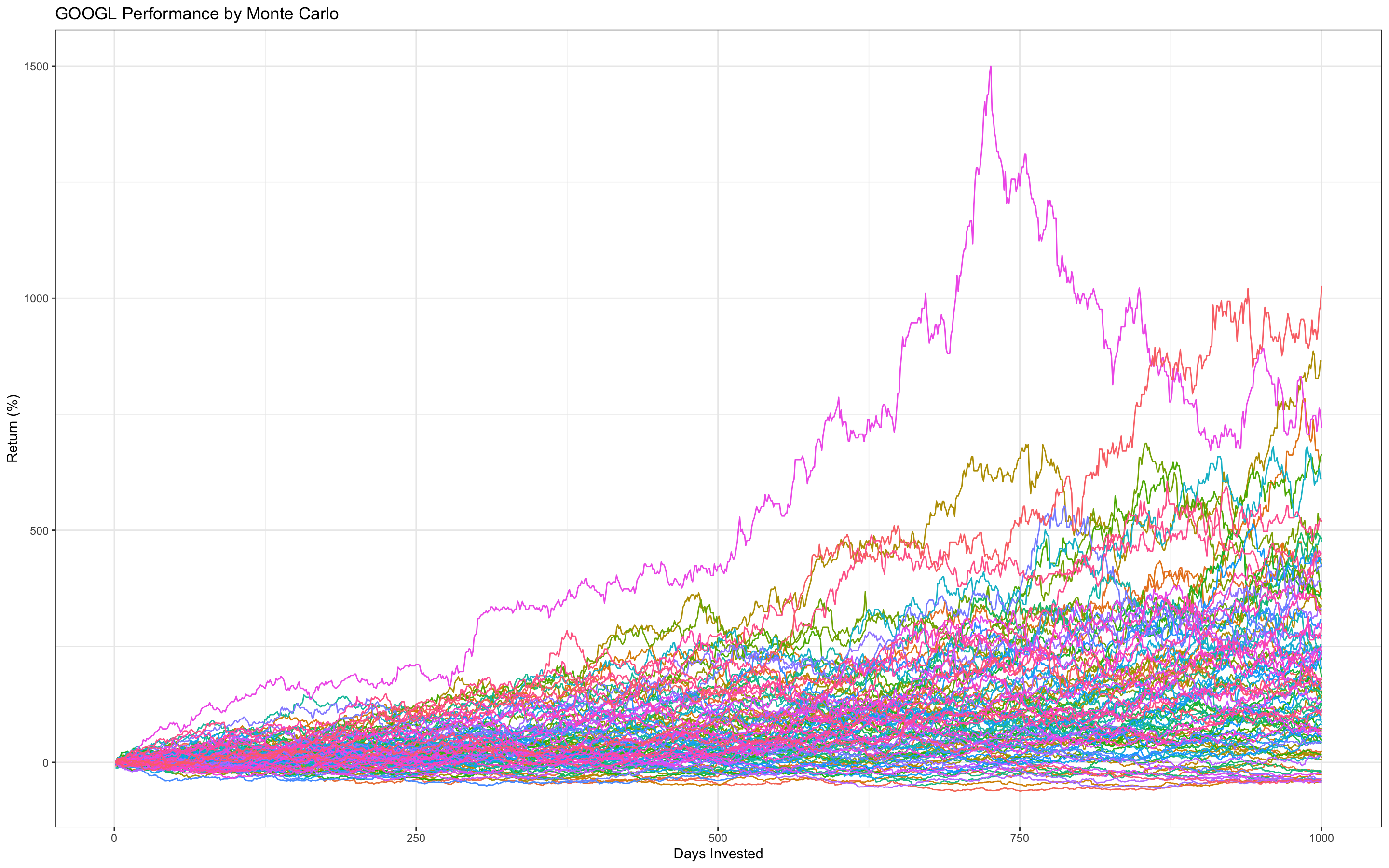

- Monte Carlo Simulation: Harness the power of Monte Carlo methods to model and simulate complex financial scenarios, providing a robust framework for risk analysis and decision-making.

For more info check: https://github.com/vladislavpyatnitskiy/Risk-Management-Analytics/wiki